Newton: 316.283.6655

Andover: 316.202.9990

.jpg)

Newton: 316.283.6655

Andover: 316.202.9990

By Dr. Robert Roeser, D.O., founder of Integrity Medicine, a Direct Primary Care practice in Newton and Andover, Kansas.

Yes. You can pay your Direct Primary Care membership with your Health Savings Account starting January 1, 2026. You can keep contributing to the account at the same time. The monthly fee must stay at or below $150 for one person or $300 for a family. The membership must cover primary care and nothing else.

We founded Integrity Medicine in 2004. We moved the practice to Direct Primary Care in 2017 after insurance rules sometimes blocked patients from care they needed. Patients asked for years whether they could use HSA money toward the membership. Until this year the answer in Kansas was no.

The tax rules changed. Money set aside in an HSA can now cover the primary care patients use most often. They keep the tax advantage while they do it.

Congress updated the tax code in Section 71308 of the One Big Beautiful Bill Act. The bill became law on July 4, 2025. The IRS released guidance in Notice 2026-05 on December 9, 2025. A public announcement followed.

For any membership that meets the federal conditions, you can pay the membership fee with HSA money, tax-free.

The law examines the membership terms themselves. Qualification does not depend on which services any one person happens to use.

A qualifying membership meets these conditions:

You can spread payments over a longer period. The yearly total must fit under the cap. For one person in 2026 that could mean $1,800 for the year, $900 for six months, or $450 for a quarter.

The core HSA rules remain in place. You still need a qualifying high-deductible health plan before you can contribute to an HSA. The 2026 change means the membership no longer disqualifies you from contributing. It does not remove the high-deductible plan requirement.

Our guide on whether you need health insurance alongside Direct Primary Care in Kansas walks through how the two fit together. https://integritymedicine.com/blog/do-you-need-health-insurance-with-direct-primary-care-in-kansas

For 2026 you can contribute up to $4,400 with self-only coverage or $8,750 with family coverage. You can add $1,000 more once you turn 55. These figures come from Revenue Procedure 2025-19.

One additional update helps people who buy their own coverage. Bronze and catastrophic plans now count as high-deductible plans for HSA purposes. The IRS confirmed they qualify whether purchased through the marketplace or elsewhere.

Your membership fee does not count toward your insurance deductible or out-of-pocket maximum. It sits outside that side of the calculation. That is part of why the cost stays predictable.

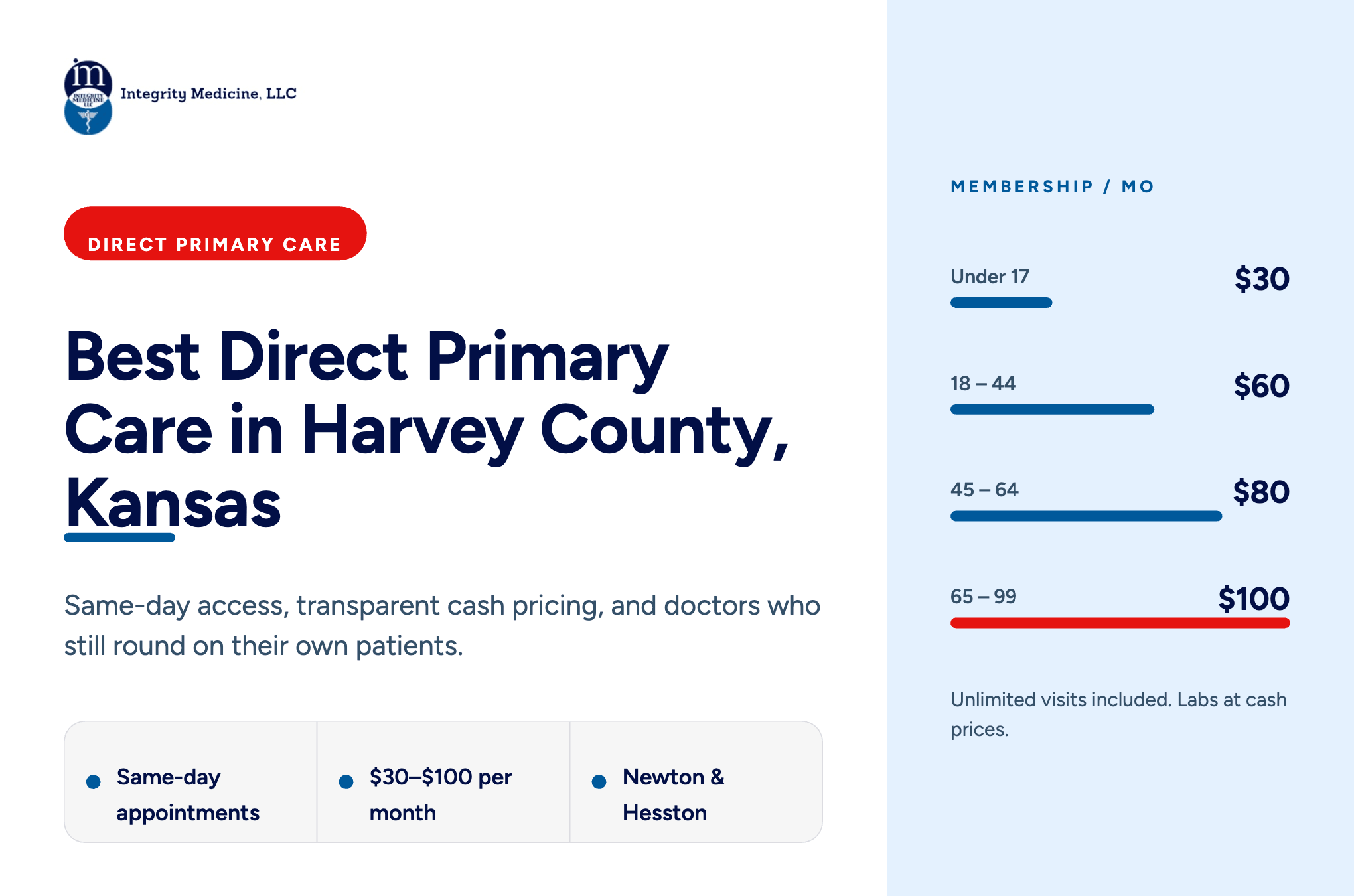

Our memberships run $30 a month for children through age 17, $60 for adults 18 to 44, $80 for adults 45 to 64, $100 for adults 65 to 99, and $1 for adults over 100 years old (you've earned it).

Every tier stays under the $150 individual cap. A family of four often totals around $180 a month. That stays under the $300 family cap. You can see what each tier includes on our membership and pricing page.

The tax savings come from the starting point of the dollars. Pay the membership from regular take-home pay and you have already paid income tax on it. Pay it from an HSA and you spend pre-tax dollars instead.

Multiply your yearly membership fee by your combined marginal tax rate. That amount is roughly what the HSA route saves.

Patients often want help comparing total costs. Most people stop at the copay. They set aside the monthly premium, the deductible they pay before insurance steps in, and the out-of-pocket maximum on top.

Add those together. A lower-premium high-deductible plan paired with a membership paid pre-tax often costs a family less than the plan they thought was covering them. Self-employed patients and small business owners across Butler and Harvey County tend to notice the difference first.

Our breakdown of Direct Primary Care versus traditional insurance in Kansas runs the comparison in full. https://integritymedicine.com/blog/direct-primary-care-vs-traditional-insurance-based-care-in-kansas

The membership fee is one piece. Much of what you receive through our office can come from HSA money as well. We bill those items on their own, outside the membership.

Medications through our wholesale generic pharmacy run about 15 percent of retail counter prices. A complete blood count that costs around $65 at standard rates runs $2.85 through us.

Labs, imaging, and minor procedures we bill separately count as qualified medical expenses. You can use HSA dollars for them on the same visit.

You can see everything the membership itself covers in our guide to what a Direct Primary Care membership includes in Kansas. https://integritymedicine.com/blog/what-does-a-direct-primary-care-membership-cover-in-kansas

A practice can offer items outside the membership and bill for them on their own. This does not put the membership's status at risk. You receive the wholesale price and the tax benefit together.

Qualification rests on how the membership is written. You cannot skip certain services and treat the rest as qualifying. The IRS addressed this in Notice 2026-05. It depends on the terms of the arrangement, not on which parts any individual uses.

Employer payments follow a different rule. If your employer covers the Direct Primary Care fee, including through a pre-tax payroll arrangement, that money already carries a tax advantage. You cannot reimburse yourself for it from your HSA. We run an employer Direct Primary Care program for Kansas businesses. We review this point with owners before they sign up.

A fee above the cap changes one thing. It stays a qualified expense you can pay from an HSA. It disqualifies you from contributing to the HSA while you remain enrolled. Our pricing keeps every tier under the limit.

Confirm you have a qualifying high-deductible health plan and an open HSA. Check your membership tier against the cap. Our pricing fits.

Pay the fee with your HSA debit card. Or pay out of pocket and reimburse yourself from the account later. Keep the receipt either way.

Run your own situation past your accountant or benefits administrator before you change how you pay. The federal rule is settled. How it applies to your plan and your taxes depends on details specific to you.

Yes. Starting January 1, 2026, you can pay a qualifying Direct Primary Care membership with HSA funds. You can keep contributing to your HSA at the same time. The fee must stay at or below $150 a month for one person or $300 for a family. Every tier at our Newton and Andover clinics meets the limit.

Yes. The rules still require a qualifying high-deductible health plan before you can contribute to an HSA. The 2026 change means your membership no longer blocks those contributions. It does not replace the plan requirement.

The 2026 law addresses HSAs. It does not speak to flexible spending accounts. FSAs follow their own rules and limits. Check with your plan administrator before you assume coverage.

A fee above $150 for an individual or $300 for a family stays a qualified medical expense you can pay from an HSA. It disqualifies you from contributing to the HSA while you are enrolled. Our tiers all fall under the individual cap.

No. Under the 2026 rules, a qualifying Direct Primary Care membership is no longer treated as a disqualifying health plan. It works alongside your high-deductible plan rather than competing with it.

If a membership fits what you need, schedule a free meet-and-greet at our Andover or Newton clinic. Bring your questions about your plan. Run the tax side past your accountant. We will handle the medicine.

Dr. Robert Roeser, D.O. founded Integrity Medicine in 2004 and converted the practice to Direct Primary Care in 2017. A board-certified internal medicine physician, he sees patients at the Newton and Andover clinics and is a member of the medical staff at Newton Medical Center.